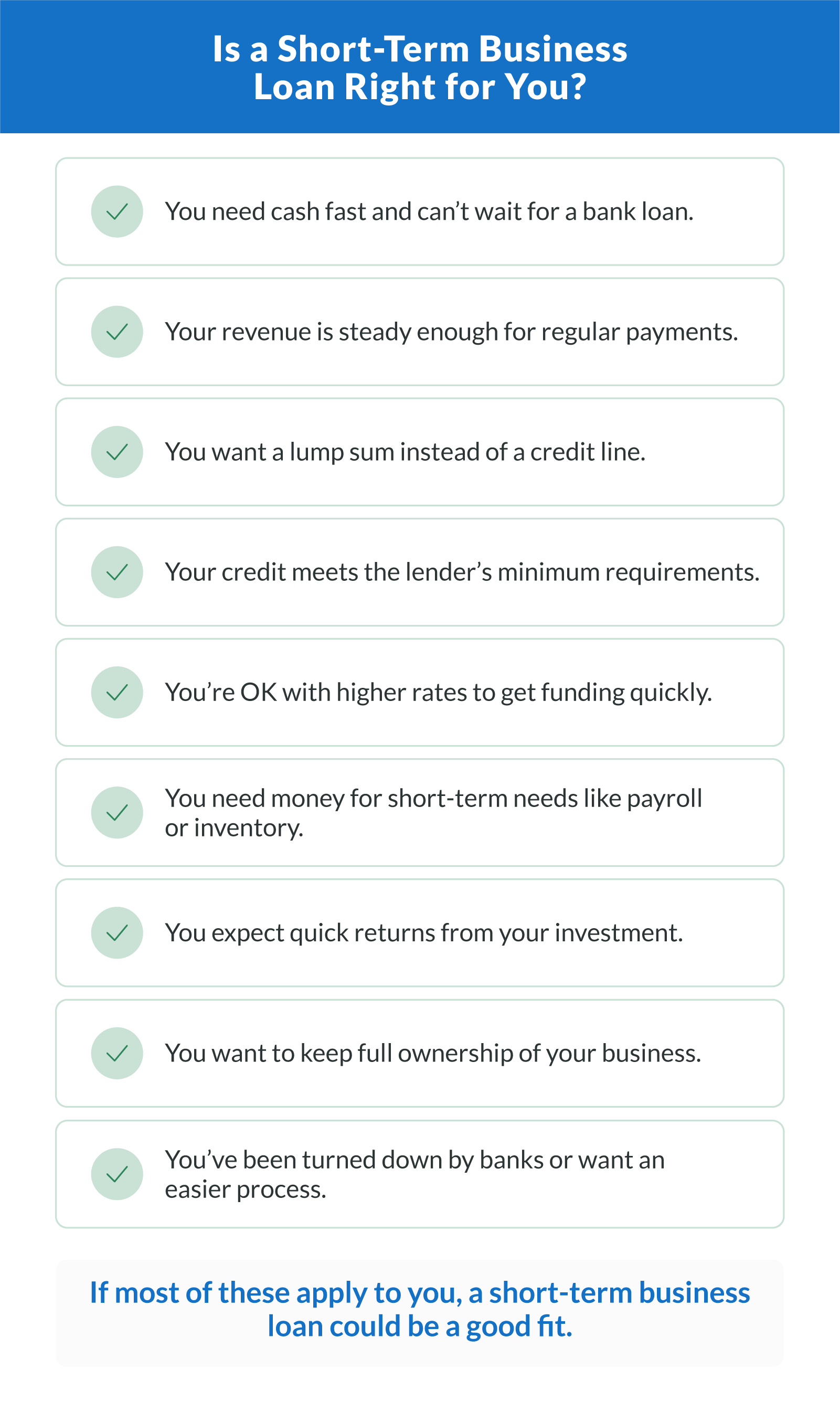

A short-term business loan gives you a fixed amount of working capital with a set interest rate and a predictable repayment schedule. You pay it back through regular monthly or weekly payments over 6 to 24 months, and most short-term loans don't require collateral.

I've spent over 15 years helping small business owners find the right business financing, and short-term loans are one of the most common solutions I recommend. They're fast, flexible, and built for businesses that need to cover cash flow gaps, handle emergencies, or act on time-sensitive opportunities without taking on years of debt. At Clarify, we structure every term loan with early payoff incentives and no prepayment penalties to keep your borrowing costs down.

When you need funding fast, a short-term loan from Clarify can put capital in your hands in as little as 24 to 72 hours. Our team will help you through the application process and lock in repayment terms that fit your cash flow.

Before you apply, compare the main types of short-term financing to find the best fit for your business needs.

| Short-Term Loan Type Comparison | ||||

|---|---|---|---|---|

| Loan type | Loan amount | Repayment terms | Interest rates | Best for |

| Short-term business loan | $10K to $500K+ | 6 to 24 months | Starting at 7% | Lump sum needs like equipment or payroll |

| Business line of credit | $10K to $1M+ | Revolving | Variable (lower rates) | Managing working capital or cash flow gaps |

| Merchant cash advance | $5K to $500K | Based on sales volume | Factor rates apply | Bad credit borrowers with strong sales |

| Invoice factoring | Up to 90% to 100% of receivables | Until invoice cleared | Fees per invoice | Businesses with unpaid invoices or slow AR |

Types of Short-Term Business Loans

Short-term business loans aren't the only way to secure fast working capital. Depending on your cash flow, credit score, and loan amount needs, other short-term business financing options may be a better fit. These lending solutions each serve slightly different purposes.

Business line of credit. A credit line offers revolving access to funds and only charges interest on what you use. It's particularly helpful for covering day-to-day working capital needs or preparing for seasonal slowdowns.

Merchant cash advance. An MCA provides a lump sum in exchange for a portion of future sales. It's a strong option if you have irregular revenue or limited personal credit.

Invoice factoring. This converts unpaid invoices into immediate cash by selling your receivables to a factoring company. It's ideal for businesses with strong accounts receivable but delayed payments.

Short-term business loan. A term loan offers fast, fixed funding with predictable repayment terms. It's ideal for covering lump sum expenses like equipment, payroll, or growth opportunities such as inventory purchases.

When comparing these financing options, consider repayment terms, factor rates, funding speed, and the impact on your business cash flow. Choosing the right product helps you meet short-term needs while protecting long-term growth.

Short-Term vs. Long-Term Business Loans

Not sure whether a short-term or long-term business loan is right for you? The answer depends on how much you need, how fast you need it, and how quickly you can pay it back.

| Short-term loan | Long-term loan | |

|---|---|---|

| Loan term | 6 to 24 months | Up to 10+ years |

| Best for | Immediate cash needs | Major investments or expansion |

| Funding speed | As fast as 24 hours through Clarify Capital | As fast as 24 hours through Clarify Capital |

| Interest rates | Usually higher interest rates | Generally lower interest rates |

| Qualification | More flexible credit score and documentation requirements | Stricter credit score and business history requirements |

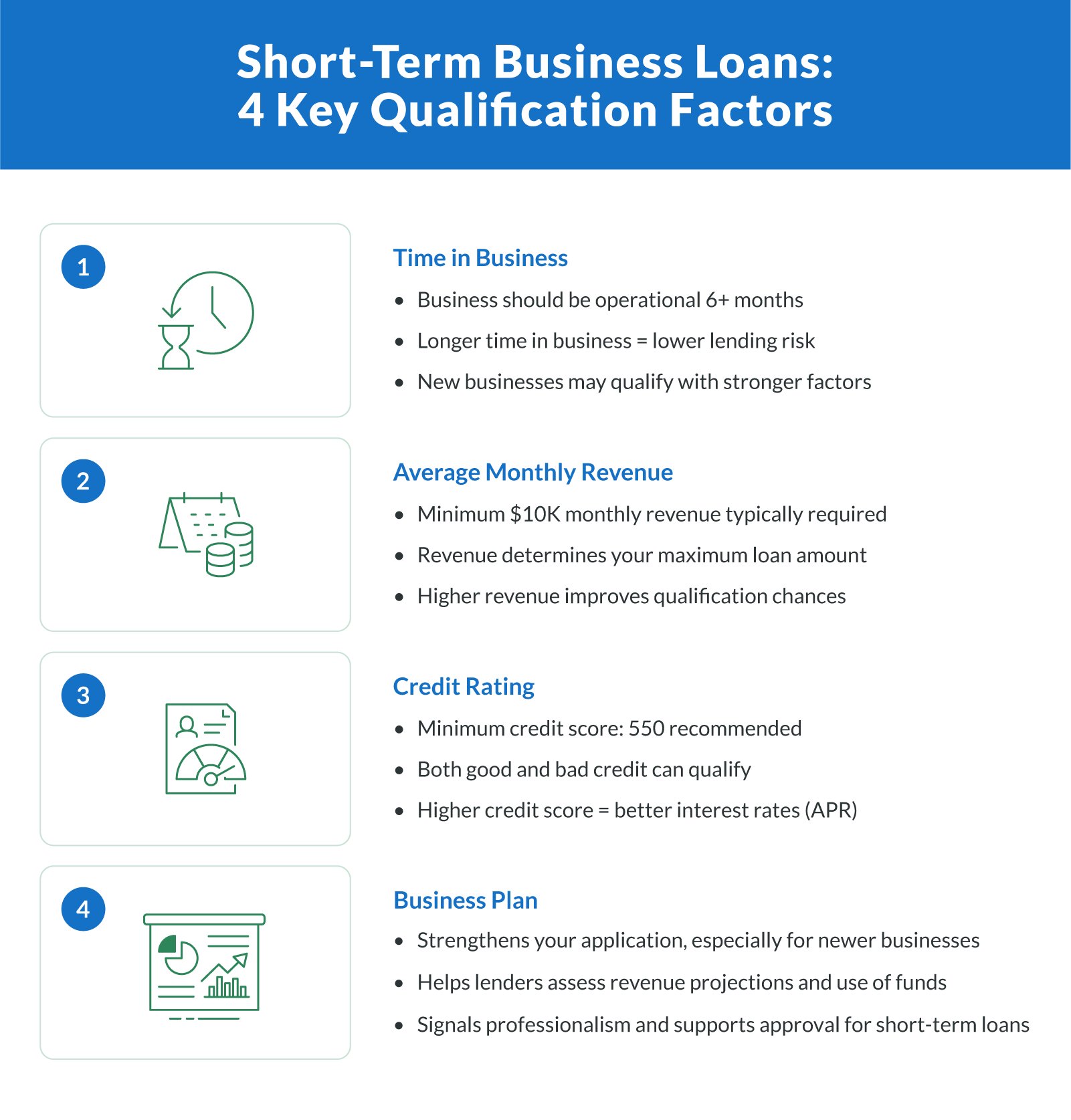

How To Qualify for a Short-Term Business Loan

Short-term small business loans are one of the fastest ways to get working capital, and qualifying is more straightforward than most business owners expect. Here's what lenders typically evaluate during underwriting to determine whether you meet their eligibility requirements.

Time in Business

New businesses can qualify, but your company should be operational for at least six months. Time in business is one of the first things lenders check because it signals stability. The longer you've been operating, the lower the risk you represent, and the easier it is to access financing.

Monthly and Annual Revenue

Clarify Capital requires your business to generate at least $10,000 per month in revenue. Your current monthly and annual revenue numbers help lenders calculate the maximum loan amount you qualify for. You'll also need to provide three to four months of recent bank statements from your business bank account to verify incoming revenue.

Credit Score and Credit History

You can get a short-term loan with both good and bad credit. Your personal credit history and credit report are among the factors that determine your interest rate. The higher your credit score, the better APR you'll typically receive.

Clarify accepts borrowers with a minimum credit score of 500, though a score of 550 or above will generally get you a stronger offer. Some lenders may also review your business credit profile to assess overall creditworthiness.

Business Plan and Documentation

Preparing a business plan that outlines your goals, revenue projections, and intended use of funds can strengthen your application. Lenders view a solid plan as a sign of professionalism and strategic thinking.

Beyond that, have these documents ready:

Three to four months of recent bank statements

Business tax returns or financial statements

Proof of business ownership and registration

Government-issued ID

Some lenders may also require a personal guarantee, which means you're personally responsible for repaying the loan if your business can't. At Clarify, most of our short-term loans are unsecured, so your personal assets aren't at risk.

Even if your credit score isn't where you'd like it to be, our Clarify advisors will guide you through to approval. To get started, complete our quick online application. Our streamlined process makes sure you can apply for funding with minimal hassle.

Need Short-Term Capital? Get Funded Fast.

Your dedicated Clarify advisor compares options from 75+ lenders to find the right short-term loan for your business. No hidden fees, no prepayment penalties.

Funding Speed

24–72 Hrs

Loan Amounts

Up to $5M

Credit Score OK

500+

Repayment Terms

6–24 Mo

How Short-Term Business Loans Work

Short-term funding from Clarify Capital starts with a simple online application. Here's how the process works:

Submit your application. Fill out a short form with basic business and financial details. The entire process takes just minutes.

Get matched with an advisor. Your dedicated Clarify advisor reviews your application, compares options from 75+ lenders, and identifies the best loan for your situation.

Review your offer. You'll receive a clear breakdown of your loan amount, interest rate, repayment schedule, and total cost. No hidden fees, no surprises.

Receive your funds. Once approved, funding can hit your account in as little as 24 to 72 hours. Some borrowers qualify for same-day funding depending on the lender and timing.

You repay the loan over a set period (typically 6 to 24 months) through weekly or monthly installments. Your loan terms, including interest rates and repayment schedule, are based on factors like your credit score, annual revenue, and overall creditworthiness.

Unlike personal loans or traditional business loans from a bank, short-term loans from online lenders prioritize speed and accessibility. Traditional banks and FDIC members might offer lower interest rates, but their loan programs often require extensive documentation and can take weeks to process. At Clarify, we streamline the process to get you fast business funding with transparent terms, up-front disclosures, and no hidden fees.

Pros and Cons of Short-Term Business Loans

Every financing option has trade-offs. Here's what to weigh before you apply.

Pros

Quick funding. Unlike traditional bank or SBA loans, short-term lenders can approve and fund your loan within one to two business days. That speed lets you address immediate opportunities or emergency expenses without disrupting operations.

Easier qualification. You can qualify for short-term financing whether you have good or bad credit. Short-term business loans are some of the most accessible loan options for small business owners.

No collateral required. With most short-term loans, you maintain full ownership of your business assets. That makes it a lower-risk financing option compared to secured loans.

Tax advantages. The interest you pay on your term loan is tax-deductible at year-end, reducing the overall cost of borrowing.

Transparent process. Your dedicated advisor walks you through every step, from terms to payment schedules, so you know exactly what to expect.

Cons

Higher interest rates. Short-term loans typically carry higher APRs than longer-term loans because lenders take on more risk with shorter repayment windows.

More frequent payments. Weekly or biweekly payment schedules can strain cash flow if you're not prepared. Make sure your revenue supports the repayment cadence before you sign.

Smaller loan amounts. If you need a large sum for a major investment (like real estate or a multi-year expansion), a long-term loan or SBA loan may be a better fit.

Shorter repayment period. Paying back a lump sum in 6 to 24 months means higher monthly payments compared to spreading the same amount over several years.