Is a small business loan an installment loan or revolving credit? The answer shapes how you borrow money, manage monthly payments, and control cash flow. Most small business loans are installment loans, meaning you receive a lump sum and repay it through fixed payments over a set repayment period. Revolving credit, such as business lines of credit and business credit cards, works differently by giving you ongoing access to available credit up to a credit limit.

This guide explains the key differences between installment loans and revolving credit, how each affects repayment structure and interest costs, and when one type makes more sense than the other for small business owners in 2026. You will also see real‑world examples by loan type and learn how lenders evaluate each option so you can choose financing that fits your business needs.

Understanding Installment Loans for Small Businesses

Installment loans are the most common type of small business financing. With installment credit, you borrow a fixed loan amount up front and repay it over a defined loan term using fixed monthly payments. The payment amount, due date, and repayment period stay the same for the life of the loan, which makes budgeting easier and supports predictable cash flow.

How Installment Loans Work

Installment loans follow a straightforward structure. You receive a lump sum at funding, then repay principal and interest together on a set schedule. Most installment loans use a fixed‑rate structure, meaning the interest rate does not change over time. This differs from revolving credit accounts, where balances and interest costs fluctuate.

Installment loans include term loans, SBA loans, equipment loans, auto loans, and even personal loans like student loans and car loans, all of which follow the same fixed‑payment model.

Common Installment Loan Use Cases

Installment loans work best for one‑time or planned expenses where the amount of money needed is clear up front. This structure works best when you have a clear repayment timeline, and your business can comfortably manage predictable payments. Here are some areas where an installment loan would be beneficial:

Equipment purchases. Financing machinery, vehicles, or technology with a fixed payment schedule.

Expansion projects. Funding renovations, new locations, or long‑term growth initiatives.

Debt consolidation. Replacing multiple high‑interest balances with one lower‑interest installment debt.

Many small businesses prefer installment loans because lower interest rates and fixed repayment periods reduce financial uncertainty.

Understanding Revolving Credit for Small Businesses

Revolving credit offers flexibility instead of structure. With a revolving line of credit, you receive access to a credit limit rather than a lump sum. You can borrow money, repay it, and borrow again as long as the account remains open and in good standing.

How Revolving Credit Works

Revolving credit accounts reset as you repay balances. Interest applies only to the amount you borrow, not the total credit limit. Monthly payments often include a minimum payment requirement rather than a fixed payment amount.

Common types of revolving credit include business lines of credit, business credit cards, personal lines of credit, and home equity lines of credit (HELOCs).

Common Revolving Credit Use Cases

Revolving credit is designed for short‑term or recurring expenses that change month to month, such as:

Working capital gaps. Cover payroll, rent, or vendor payments during slow periods.

Seasonal inventory. Buy inventory ahead of peak sales cycles.

Unexpected expenses. Handle emergency repairs or urgent operating costs.

Because available credit replenishes as you repay, revolving credit accounts provide ongoing financial flexibility.

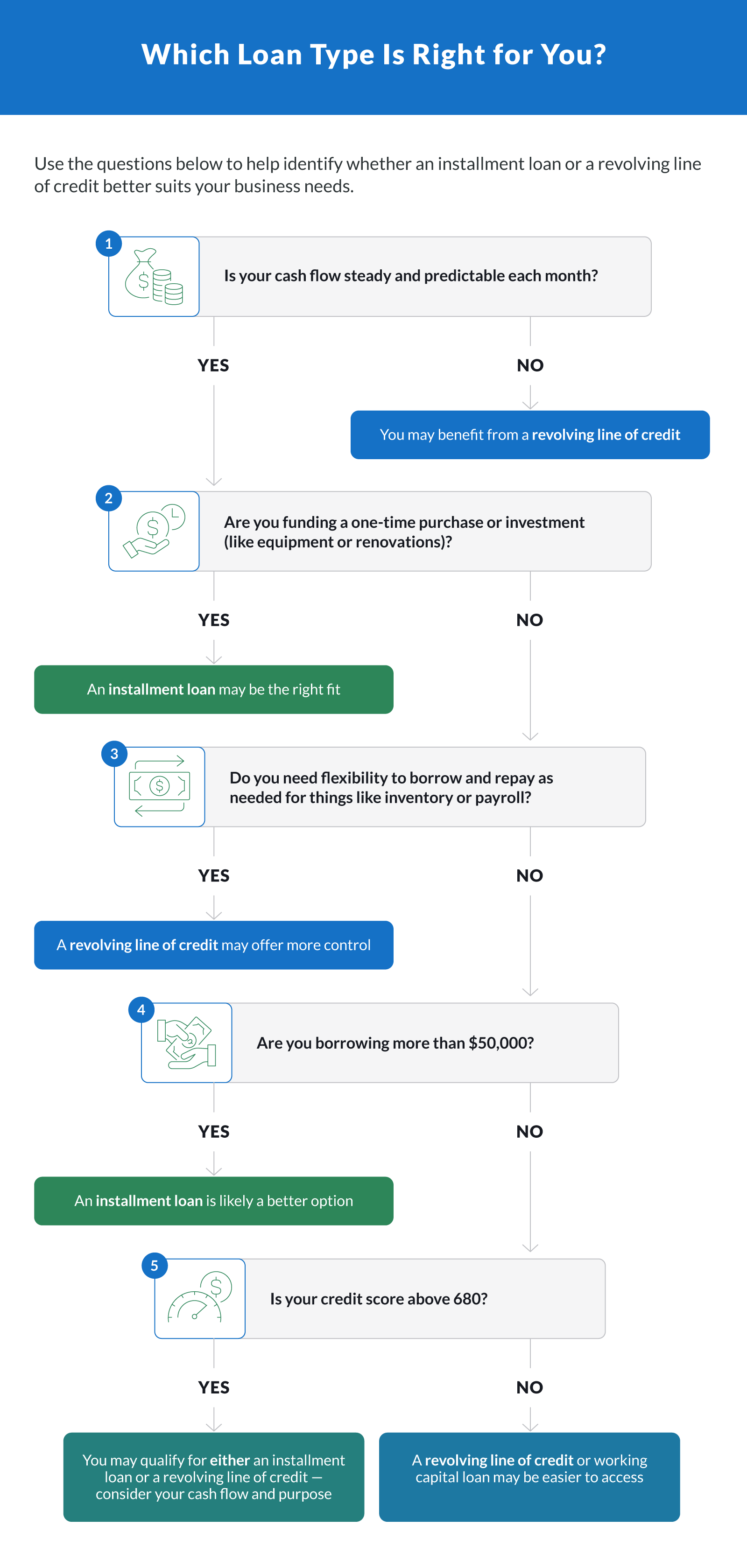

Installment Loans vs. Revolving Credit: Key Differences

Choosing between installment loans and revolving credit comes down to repayment structure, flexibility, and predictability.

| Comparison Table: Installment vs. Revolving Credit | ||||

|---|---|---|---|---|

| Loan type | Repayment structure | Interest rate | Flexibility | Best for |

| Installment loan | Fixed payment over a set repayment period | Usually lower, often fixed‑rate | Low | Large purchases, long‑term investments |

| Revolving line of credit | Variable payments with a minimum due | Variable interest rate | High | Ongoing expenses, cash flow management |

| Business credit card | Minimum payment or full balance | Highest variable APR | Very high | Small recurring expenses, emergencies |

Pros and Cons of Each Loan Structure

Both types of credit serve important roles in business finance, but each comes with tradeoffs.

Installment Loan Pros and Cons

Each loan structure supports different business goals — but understanding the tradeoffs helps you choose the one that fits your financial strategy.

The pros of an installment loan include:

Predictable monthly payments and fixed due dates

Typically lower, fixed interest rates

Easier long‑term planning and budgeting

Great for large, one-time expenses

Builds repayment discipline

Here are some of the cons:

Less flexibility once terms are set

Harder to adjust repayment if cash flow changes

May have stricter credit or income requirements

Funds cannot be reused after repayment

Revolving Credit Pros and Cons

Revolving credit gives you flexibility and control, but it also requires careful management to avoid costly pitfalls.

Here are the pros:

Flexible borrowing; draw only what you need and reuse available credit

Credit replenishes as you repay

Quick access to working capital

No need to reapply for every withdrawal

Useful for unexpected or recurring expenses

Interest applies only to borrowed balances

Helpful for variable or seasonal cash flow

The cons include:

Higher interest rates and variable APRs

Can be harder to budget due to rate fluctuations

High credit utilization can affect credit score

Examples by Loan Type

Understanding how each loan works in practice clarifies the decision.

Installment Loan Examples

A construction company finances a work truck using a five‑year installment loan with a fixed payment. A restaurant owner takes out a term loan to renovate a kitchen and repays it over 36 months. A retailer uses an SBA 7(a) loan to purchase real estate with a long repayment period.

Revolving Credit Examples

An e-commerce brand uses a revolving line of credit to fund digital ads and repays balances weekly. A consulting firm relies on a business credit card for travel expenses and pays it in full each month. A seasonal business draws from a credit line during slow months and repays during peak sales.

Interest Rates, Repayment, and Credit Impact

Loan structure affects more than payments. It also shapes credit history and long‑term borrowing power.

Installment loans typically offer lower interest rates and fixed payments, which helps build a strong payment history. Revolving credit affects credit utilization, a key factor in credit reports from agencies like Experian. High balances relative to credit limits can raise borrowing costs or limit future approvals.

Using both types responsibly can help build credit, as long as payment history stays positive and balances remain manageable.

How Lenders Decide Which Option You Qualify For

Lenders evaluate different factors depending on the loan type. Installment loans focus on credit score, revenue stability, repayment ability, and loan term fit. Revolving credit places more emphasis on cash flow consistency, payment history, and credit utilization patterns.

Most online lenders now offer soft credit checks during prequalification, allowing borrowers to compare loan options without harming their credit report.

How To Choose the Right Loan Type for Your Business

Choosing the right structure depends on how you plan to use the funds.

If you need a set amount of money for a defined purpose, installment loans provide stability and lower long‑term costs. If your expenses fluctuate or you want ongoing access to capital, revolving credit offers flexibility.

Many businesses use both an installment loan for long‑term investments and a revolving line of credit for short‑term cash flow.

Choosing the Best Loan Structure for Your Business

The difference between installment loans and revolving credit comes down to structure versus flexibility. Installment loans deliver predictability with fixed payments and lower interest rates, while revolving credit provides reusable access to funds when cash flow changes.

Understanding these differences helps you borrow responsibly and align financing with your business goals. Clarify Capital works with business owners to compare loan types, repayment terms, and lender options side by side.

Apply today in minutes to see whether an installment loan, revolving line of credit, or a combination of both fits your business best.

Frequently Asked Questions

Still have questions about how installment loans and revolving credit work? These quick answers cover the most common points business owners ask about loan types, rates, and how they compare.

Is a Small Business Loan Usually an Installment or a Revolving Loan?

Most small business loans are installment loans. Revolving credit is typically used for working capital rather than major purchases.

Is a Business Credit Card Considered Revolving Credit?

Yes. Business credit cards are revolving credit accounts with a credit limit and a minimum payment requirement.

Which Option Has Lower Interest Rates?

Installment loans usually have lower interest rates than revolving credit, especially compared to credit cards.

Can Revolving Credit Become Installment Debt?

Some lenders allow refinancing a revolving balance into an installment loan, which can lock in fixed payments and lower rates.

Does Revolving Credit Hurt My Credit Score?

It can if balances remain high. Credit utilization plays a major role in credit scoring models.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts