SBA Microloans provide small business owners and nonprofits with accessible funding to support growth. Backed by the U.S. Small Business Administration, these loans offer low interest rates, flexible repayment terms, and technical assistance to help businesses succeed.

Unlike traditional small business loans, SBA Microloans are not issued directly by the government; instead, the SBA partners with intermediary lenders to distribute the funds. This loan program is ideal for businesses needing working capital, equipment purchases, or inventory, but you can't use it for real estate or to refinance existing debt.

The SBA 7(a) loan is another popular SBA-backed option, but it differs from microloans in loan size and usage. While SBA Microloans max out at $50,000, the SBA 7(a) loan can provide up to $5 million. Businesses interested in applying for an SBA Microloan should start with a microloan application through an approved lender.

Read on for all you need to know about the SBA microloan program and decide if it's the right funding option for your business.

What Is the SBA Microloan Program?

The SBA Microloan Program gives small business owners and nonprofit organizations access to funding through a network of intermediary lenders. Unlike traditional banks, these microlenders receive capital from the Small Business Administration and distribute it to eligible borrowers. This loan program is designed to help for-profit businesses and nonprofit community-based organizations that may not qualify for conventional financing options.

The program supports a variety of business needs, including working capital, equipment purchases, and expansion efforts. However, funds cannot be used to pay off existing debts or purchase real estate. Eligibility requirements vary by lender, but most borrowers must demonstrate financial responsibility and a viable plan for repaying the loan. Entrepreneurs, including those from underserved communities, can benefit from the program's flexible terms and technical assistance.

Who Qualifies for an SBA Microloan?

To qualify for an SBA Microloan, applicants must meet specific eligibility requirements. Lenders consider factors such as business history, financial projections, and credit score to determine whether a borrower is a good fit.

While requirements vary by lender, typical qualifications include:

A strong business plan. Applicants may need to provide a detailed plan outlining their company's goals, financial needs, and strategy for growth.

A reviewable credit history. Lenders evaluate the borrower's credit report to assess financial responsibility, though a minimum credit score is not always required.

Demonstrated financial projections. Businesses must show their ability to generate revenue and make consistent loan payments.

A viable business structure. Both new businesses and startups may qualify as long as they can demonstrate sustainability.

Entrepreneurship in underserved markets. Minority-owned businesses and those in low-income communities are encouraged to apply.

Willingness to provide collateral or a personal guarantee. Some microlenders may require additional financial security depending on the loan amount.

Lenders assess each application individually, considering factors beyond just a credit score. Small business owners who don't meet traditional bank loan criteria can still secure business financing through this program.

Loan Amounts

To determine how much a business can borrow through the SBA Microloan Program, lenders evaluate several factors. While the maximum microloan amount is $50,000, the average microloan is around $13,000. The exact loan amount depends on:

Business needs. Lenders assess how much funding is required for operations, inventory, equipment, or expansion.

Cash flow. A company's revenue and expenses help determine its ability to repay the loan.

Financial health. Businesses with stable earnings and strong financial projections may qualify for larger loan amounts.

Lender discretion. Each SBA-approved microlender sets its own lending guidelines and limits.

Since these loans are issued through nonprofit intermediary lenders rather than traditional banks, eligibility requirements, and loan terms may vary. Small businesses looking for flexible financing options often find SBA Microloans to be a valuable funding solution.

How You Can Use an SBA Microloan

SBA Microloan funds can be used to support various small business expenses, helping entrepreneurs manage and grow their operations. Approved uses include:

Purchasing equipment

Covering operating expenses

Increasing working capital

Many businesses use these funds to buy inventory, invest in marketing, or upgrade technology.

However, SBA Microloans cannot be used for real estate purchases or to pay off existing debts. Borrowers looking to acquire commercial property or refinance loans may need to explore other financing options.

While the program allows funding for general business assets and operational costs, it is designed to support business growth rather than debt consolidation.

Interest Rates and Repayment Terms

SBA Microloan interest rates are typically lower than those of traditional bank loans, making them an affordable financing option for small businesses. Rates vary depending on the lender but generally fall between 8% and 13%. Clarify Capital offers competitive loan rates as low as 7%.

Repayment terms on SBA Microloans range from six months to six years, depending on the loan amount and the borrower's financial situation. Monthly payments are required, and lenders assess factors like business credit, cash flow, and loan use to determine terms. Closing costs may apply, but they are usually lower than those associated with larger loans.

Since these loans are provided by nonprofit microlenders rather than banks, they often offer more flexible terms for businesses that do not qualify for traditional financing.

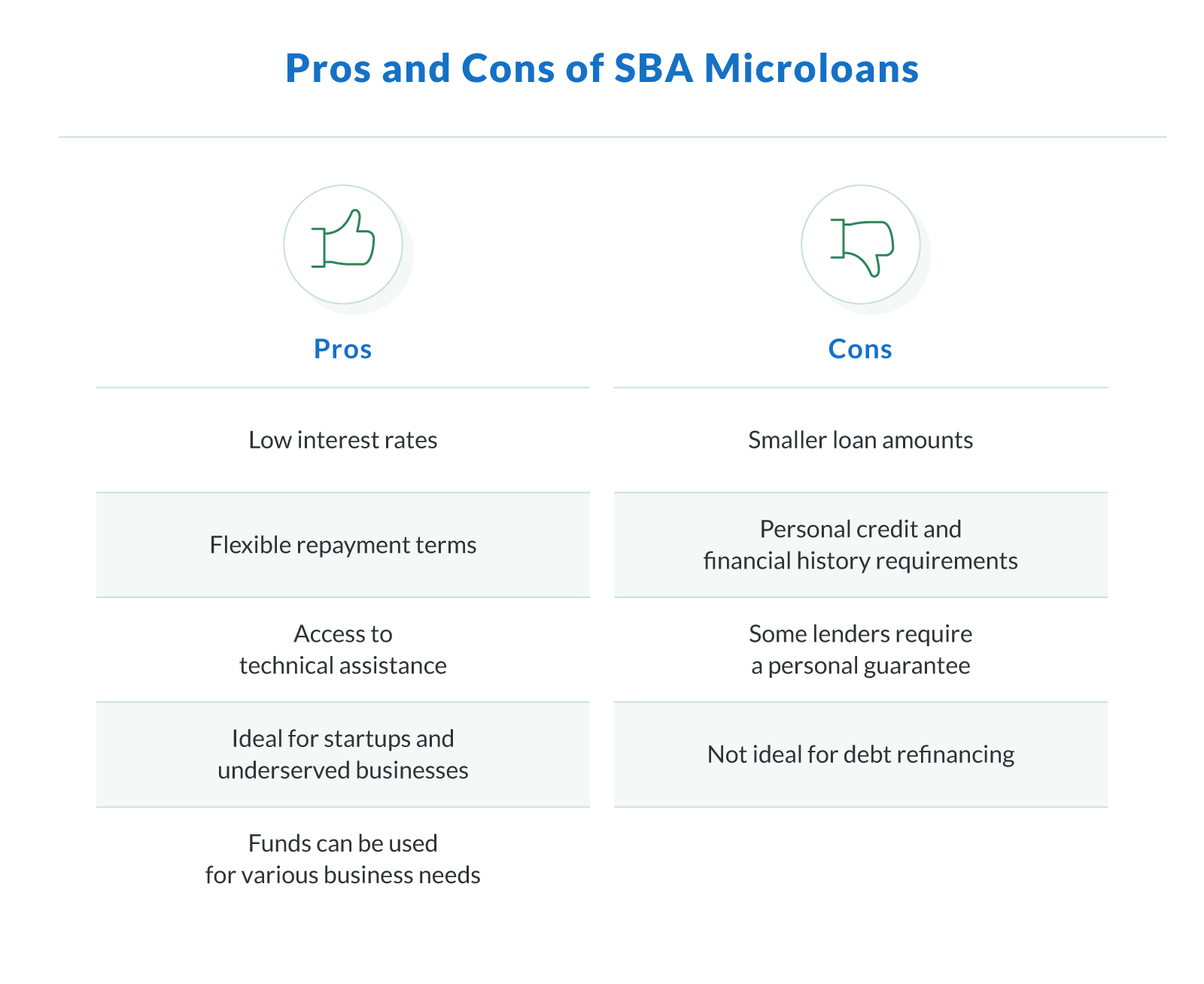

Pros and Cons of SBA Microloans

SBA Microloans offer small business owners an accessible financing option with competitive terms, but they also come with some limitations. Understanding both the benefits and drawbacks can help businesses determine if this loan program is the right fit.

Pros of SBA Microloans

SBA Microloans provide several advantages that make them a great choice for entrepreneurs looking for affordable business financing.

Low interest rates. Compared to many alternative funding options, SBA Microloans offer lower rates, making repayments more manageable.

Flexible repayment terms. Borrowers can secure repayment terms of up to six years, depending on their financial situation and loan use.

Access to technical assistance. Many SBA-approved microlenders provide training and guidance to help businesses succeed.

Ideal for startups and underserved businesses. Small businesses that don't qualify for traditional bank loans can access funding through this program.

Funds can be used for various business needs. Entrepreneurs can use SBA Microloan funds for equipment, inventory, and working capital.

Cons of SBA Microloans

While SBA Microloans are a valuable financing option, they have some limitations that may not work for every business:

Smaller loan amounts. The maximum loan amount is $50,000, which may not be enough for businesses with larger financing needs. Companies that require substantial funding for major expansions, large equipment purchases, or real estate investments may need to explore other financing options such as SBA 7(a) loans or traditional bank loans.

Personal credit and financial history requirements. Clarify Capital works with lenders that consider multiple factors when approving SBA Microloans. While personal credit is evaluated, a strong business plan, revenue, and overall financial health also play a role. Some lenders may approve borrowers with less-than-perfect credit if they demonstrate strong business performance and repayment ability. Your Clarify Capital advisor will help match you with the best financing option based on your situation.

Some lenders require a personal guarantee. Clarify Capital works with a variety of lenders, and some SBA-approved microlenders may require a personal guarantee or collateral depending on the loan amount and the borrower's financial profile. Your dedicated Clarify Capital advisor will help you understand the specific requirements for your loan and guide you toward the best financing option for your business.

Not ideal for debt refinancing. You can't use SBA Microloans to pay off existing business debts or personal loans. Alternative funding options like term loans or business lines of credit may be more suitable for consolidating debt or refinancing high-interest credit.

How To Apply for an SBA Microloan

Applying for an SBA Microloan through Clarify Capital is fast and simple. Here's how it works:

Apply online. Complete a quick, no-obligation application at Clarify Capital in under two minutes.

Get matched with a lender. Clarify works with over 75 lenders to find the best SBA-approved microloan options for your business.

Work with your dedicated loan advisor. Your Clarify Capital advisor will guide you through the entire process and help you choose the best loan terms.

Receive funding fast. Once approved, funds can be available in as little as 24 hours.

Clarify Capital makes securing an SBA Microloan easy by handling the process from start to finish. With personalized support and access to multiple lenders, small business owners can quickly get the financing they need.

Is an SBA Microloan Right for Your Business?

SBA Microloans are best suited for small businesses and entrepreneurs who need smaller amounts of funding for operational expenses, equipment, or inventory. This loan program is particularly beneficial for startups, minority-owned businesses, and nonprofit childcare centers that may struggle to qualify for traditional financing. If your business meets the eligibility requirements and needs funding to support short-term or growth-related expenses, an SBA Microloan could be a great option.

To get started, research microloan lenders and begin the application process. Clarify Capital simplifies this by matching you with the best lender for your business needs. If you're ready to apply, start your loan application today.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts